July 17, 2025

.png)

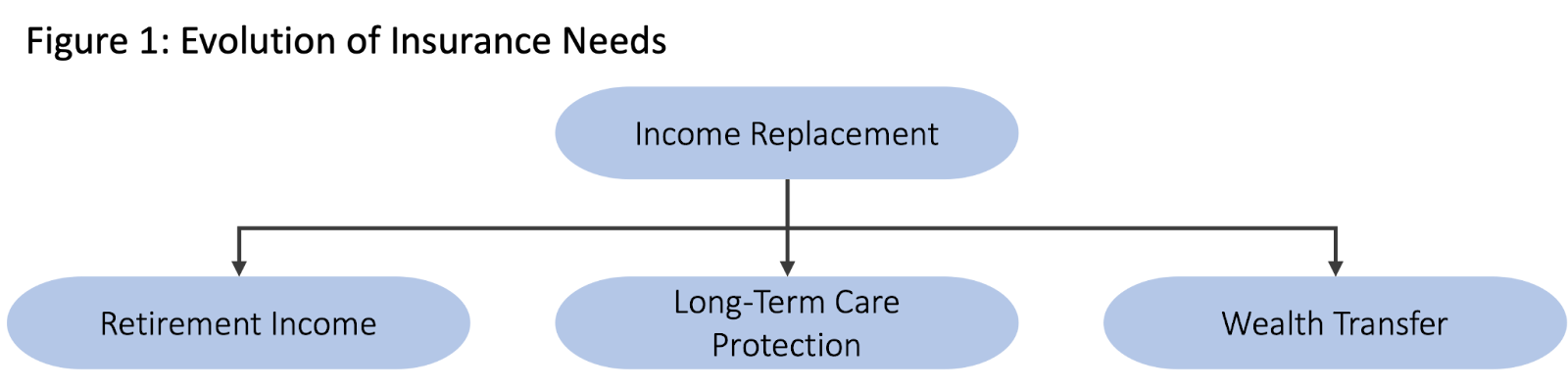

As clients approach retirement, life insurance often evolves from a safeguard against lost income to an avenue for preserving wealth and supporting new priorities. What once served a single purpose — protecting loved ones — now offers much more value.

Over time, life insurance assets accumulate significant cash value. But that value tends to sit idle, misaligned with the client’s financial aspirations. Advisors may recognize this mismatch but hesitate to take action due to perceived tax risks or limited product options. But with the right approach, that policy can become the foundation to crafting a more customized, tax-efficient strategy.

The Challenge

Advisors often face a familiar dilemma: the client's needs have changed, but the policy hasn't. Maybe retirement is approaching quickly, or health concerns are getting more pressing. That aside, the client may want to ensure their insurance dollars are doing more than just sitting in reserve.

In these moments, there’s rarely a one-size-fits-all product that checks every box. Income, healthcare, and legacy goals typically pull in different directions. Consolidating everything into a single new contract may leave some needs underserved or introduce unnecessary complexity.

Splitting the cash value among multiple, better-aligned solutions could yield a stronger result. Still, that path typically requires surrendering the current policy, potentially exposing the client to immediate tax liability on the gains. The fear of creating an avoidable tax bill stalls action, even when better-fit options are available.

The Solution

Fortunately, some insurance carriers offer the flexibility to accept split 1035 exchanges, letting clients reallocate the accumulated value of an existing policy across multiple solutions without surrendering the tax advantages they’ve already earned.

This strategy is beneficial when planning for clients who have financial priorities beyond just protection — with the proper structure, one policy can be divided into targeted products that support income, long-term care, and legacy objectives.

Our Compact Case Study

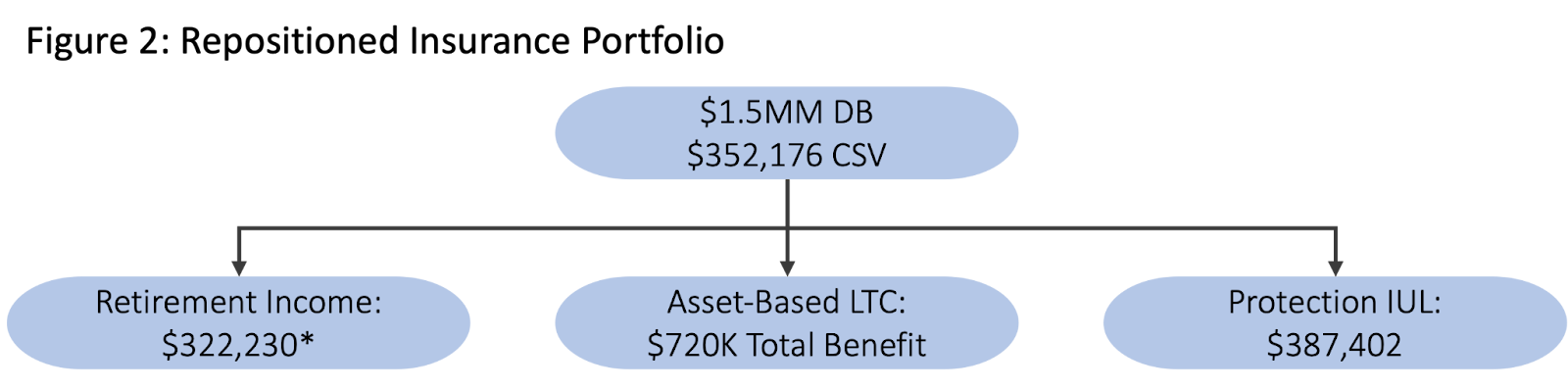

Consider a 57-year-old male holding $1.5 million in life insurance assets with a surrender value of $352,176. Instead of defaulting to a like-for-like replacement, the advisor proposed a split exchange strategy to realign the policy’s cash value to meet distinct needs:

- Protection IUL: A portion of the value was directed toward an indexed universal life policy that continues to provide a tax-free death benefit, preserving the legacy aspect of the original policy while giving the client ongoing protection.

- Asset-Based Long-Term Care (LTC) Policy: Another segment was allocated to cover potential healthcare expenses later in life. This coverage is increasingly important for clients in their 50s and 60s, especially those looking to safeguard assets without relying on family or liquidating investments.

- Annuity: The remainder was used to fund an annuity designed to produce a guaranteed lifetime income, adding a stable and predictable stream to the client’s retirement income plan.

By reallocating the policy through a split 1035 exchange, the client gained more protection from tax without sacrificing benefits. If long-term care is never needed, the combined death benefit from the Protection IUL and LTC policy totals $627,402, with no further premiums required. At the same time, the annuity guarantees more than $322,000 in lifetime income, providing $10,741 per year for 30 years, starting at age 66.

If long-term care does become necessary, the combined value of benefits, encompassing both income and care, can reach $1,429,632. This option preserves flexibility, honors the original policy’s intent, and provides overall peace of mind. For advisors, it’s a chance to turn a single conversation into a multifaceted solution, and for clients, it’s proof that insurance can still grow with them.

Let Seasoned Policies Lead to Stronger Client Outcomes

Connect with LIFE Brokerage for personalized split exchange strategies backed by our team of experienced underwriters, analysts, and case managers. We simplify the complex, save you time, and help you present client-ready recommendations with confidence. Whether managing one case or an entire portfolio, we’ll provide guidance to help your clients’ life insurance assets align with their financial goals.

-1.png?length=360&name=Option%202%20(4)-1.png)