June 12, 2025

-1.png)

As financial advisors, leveraging accumulation-focused insurance policies with significant cash value can be a powerful repositioning strategy. The goal is to align a client’s insurance portfolio with their evolving financial needs while optimizing the benefits of modern insurance products.

Proper insurance planning extends beyond securing the best underwriting offer or the lowest premium. It requires a dynamic approach that considers how insurance needs evolve over time. A comprehensive risk management strategy should address more than just survivor income or estate tax liquidity; it should also account for the escalating costs of Long-Term Care (LTC), which can threaten retirement security and erode the intended legacy.

This insight is particularly relevant given industry trends. However, simply layering a new LTC Insurance policy onto a client’s existing insurance assets may not be the most effective approach. Instead, financial advisors should explore opportunities within existing policies that no longer align with client objectives. Specifically, a personally owned life insurance policy with high cash value but outdated features can be a funding source for a modernized insurance strategy. The key challenge is repositioning these cash values efficiently for maximum client benefit.

The Efficiency vs. Benefit Dilemma

Balancing efficiency with maximizing benefits can be complex. An efficient strategy minimizes costs, including premium outlay and taxation, typically favoring a 1035 exchange. However, a conventional 1035 exchange limits product choice to single life policies on the same insured. By splitting the exchange to fund multiple policies — one for legacy planning and another for LTC coverage — clients can unlock superior benefits while maintaining tax efficiency.

A more advanced approach follows a two-step process:

1035 Exchange: The existing policy is exchanged for a new policy with enhanced benefits.

Policy Loan Strategy: The cash-rich new policy funds an updated strategy for the spouse through a policy loan, ensuring comprehensive coverage without additional out-of-pocket costs.

While policy loans can pose risks by affecting long-term policy performance, planned repayment through a structured withdrawal (within cost basis limits) mitigates this concern. The result is two policies, one for each spouse, offering death benefits for heirs and accessible LTC funds if needed.

Implementing the Strategy

Considering the following scenarios may provide additional clarity:

Client Profile:

- 65-year-old couple

- Husband owns a permanent life insurance policy with a $400K surrender value

- Wife has no permanent life insurance policy

The Conventional Solution:

- 1035 Exchange into a new policy on the husband’s life with LTC benefits

- Separate LTC policy for the wife, funded from other assets

- Alternative option: Surrender existing policy, incur tax liabilities, and fund a joint policy

The Enhanced Strategy:

- 1035 Exchange funds a new policy on the husband’s life

- A policy loan from the new policy funds coverage for the wife

- Loan repayment is structured via a planned withdrawal

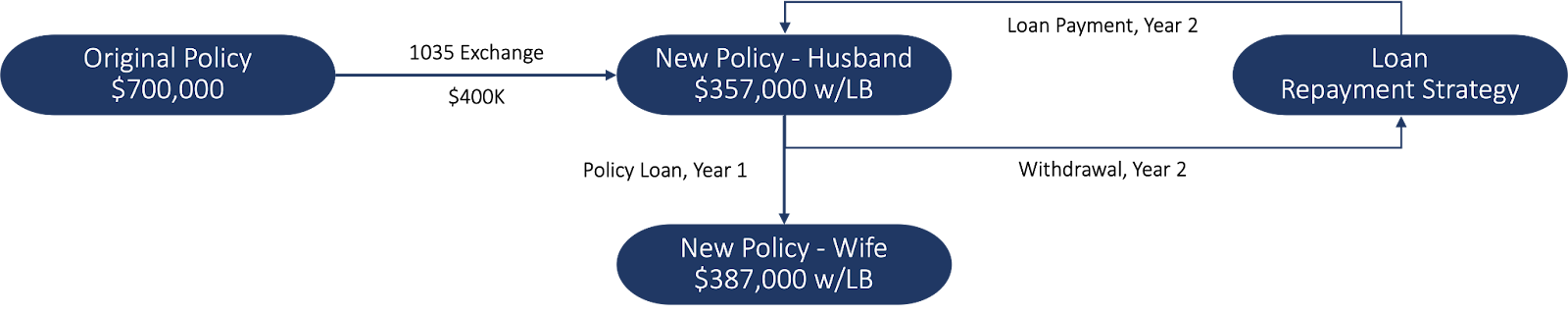

This strategy maintains policy health and eliminates long-term loan balance concerns. The figure below illustrates the fund flow, emphasizing the importance of rapid loan repayment.

While initial account values may be lower post-transaction, projections indicate that combined account values surpass $400K by year ten, and the loan balance is eliminated by year two. Importantly, this solution incurs no tax liabilities and achieves a substantial coverage upgrade.

Turning Legacy Policies Into Modern Value

Traditional insurance solutions often fall short as clients approach retirement with cost concerns and evolving priorities. This strategy offers a practical path forward: transforming underperforming policies into modern coverage that meets legacy and LTC needs, without triggering taxes or increasing out-of-pocket costs. It’s a smarter use of existing assets that strengthens client outcomes across the board.

If you’re working with clients who could benefit from this type of repositioning, contact LIFE Brokerage to discuss how we can help structure the right solution.

-1.png?length=360&name=Option%201%20(2)-1.png)

.png?length=360&name=Option%202%20(5).png)